Mapletree Logistics Trust (MLT) is a pure play pan-Asian logistics REIT whose properties are built according to modern building specifications. Warehouses used to be just another ‘boring’ property class. But with the rise of e-commerce, warehouses are given a new lease of life as they can now ride this secular growth opportunity.

MLT appears to be relatively untouched by COVID-19 as rental income from e-commerce companies continue to stream in during this crisis. MLT also has a diversified tenant base that offers it some resiliency against a recession. To see if my hypotheses are true, I tuned in to MLT’s 2020 virtual AGM to find out more.

So here are six things I learned from MLT’s 2020 AGM:

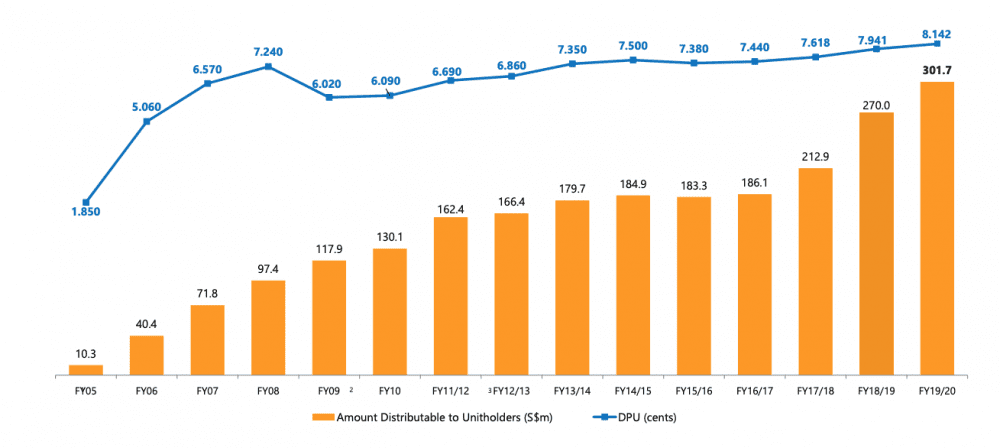

1. MLT’s distribution per unit (DPU) increased by 2.5% y-o-y in FY19/20. The increase in DPU was due to an increase in contributions from existing properties, newly acquired properties, and distribution of divestment gains. In Q1 FY19/20, Phase 1 of Mapletree Ouluo Logistic Park China completed its redevelopment; and in FY18/19, MLT made property acquisitions in Singapore, Australia, South Korea, and Vietnam.

This overall increase in DPU was partly offset by the absence of contributions from divested properties and higher borrowing costs. MLT’s DPU has risen quite steadily over the past fifteen years. However, the management said that it was unable to provide a DPU forecast due to economic uncertainties in FY20/21.

Source: Mapletree Logistics Trust 2020 AGM presentation slides

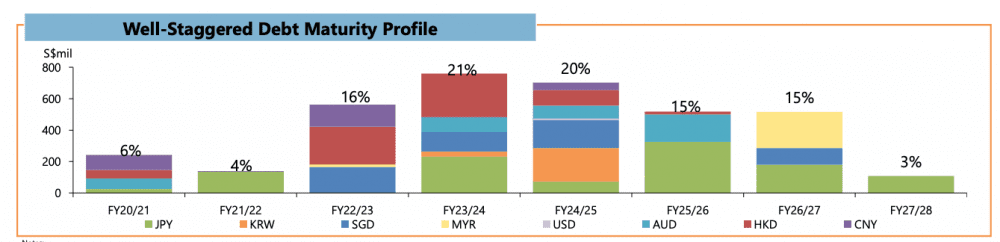

2. As at 31 March 2020, MLT’s aggregate leverage ratio is at 39.3%, a 1.6% increase y-o-y. Although still below the gearing ratio limit of 50%, MLT’s gearing ratio is relatively high compared to other SGX-listed industrial REITs. However, the management noted that it was comfortable with a current gearing level of around 40%. For sizable acquisitions in the future, MLT would consider equity raising for funds.

MLT’s interest coverage ratio stands at 4.9. As a rule of thumb, I prefer REITs with an interest coverage ratio of at least 5.0. This means that the REIT can service the interest incurred on its debt at least five times with its net property income generated during the same period as the interest was incurred. MLT’s debt maturity profile is quite well-staggered with no more than 21% of its debt expiring in a single financial year.

Source: Mapletree Logistics Trust 2020 AGM presentation slides

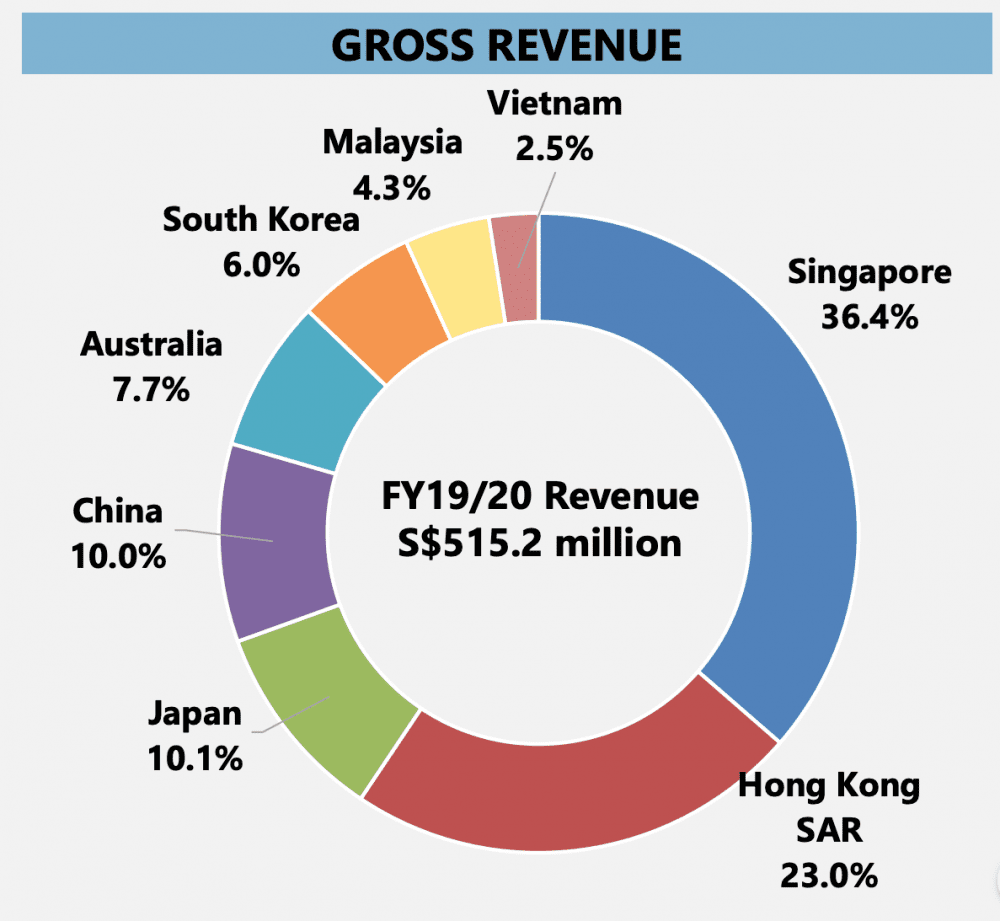

3. MLT derives its revenue from geographically diversified sources. Its top five sources of revenue by geography are Singapore (36.4%), Hong Kong (23.0%), Japan (10.1%), China (10.0%) and Australia (7.7%). Together, they account for 87.2% of MLT’s gross revenue.

Source: Mapletree Logistics Trust 2020 AGM presentation slides

Geographic diversification is becoming more important in an increasingly complex world that needs to grasp with the vagaries of US-Sino relations (especially in trade) and black swan events like COVID-19. These two defining events of the decade have led to structural shifts in global supply chains as companies relocate their production bases from China to Southeast Asian countries like Vietnam and Malaysia.

So although MLT derives 10.0% of its gross revenue from China, it shouldn’t be too badly affected by the shocks in supply chains as it also derives 6.8% of its revenue from Vietnam and Malaysia combined.

4. MLT continued to rejuvenate its portfolio through acquisitions, divestments and redevelopments in FY19/20. In FY19/20, MLT made acquisitions totalling S$752.8 million. It acquired nine high-quality modern logistics properties in Malaysia, Vietnam, China, South Korea, Japan, and Australia. These acquisitions deepen MLT’s presence in these markets and have strengthened the portfolio’s quality.

MLT divested six dated properties totalling S$275.3 million in value located mainly in Japan. It also completed the development of the Mapletree Ouluo Logistics Centre in China for S$70.0 million in May 2020, increasing its GFA 2.4 times to 80,700 square metres.

5. MLT CEO Ng Kiat said that MLT’s portfolio restructuring offers resiliency against the fluid COVID-19 situation. For example, over the past years, MLT has moved away from tenants in the more volatile import/export business to the more stable domestic consumption business. As at 31 March 2020, about 75% of MLT’s portfolio (by gross revenue) serves consumer-related sectors.

MLT has also built a network effect that is agnostic of the country its properties are located in. It seeks to strategically position its properties such that they are close to its customers, improving the efficiency in the flow of goods that were stored in MLT’s warehouses. MLT has also actively moved away from single tenant leases to multi-tenant leases.

6. The CEO believes that MLT is well-positioned with a quality portfolio and strong regional network once the COVID-19 crisis stabilises. The pandemic will only accelerate pre-existing structural trends that increase demand for modern logistics spaces. These trends include the growth of e-commerce, diversification of supply chains, and rising automation. Over the past years, MLT has continually sought to diversify its geographic base and acquire modern, high-quality logistic properties to ride these secular trends.

The fifth perspective

Mapletree Logistics Trust is one of the few stocks that has benefited from the COVID-19 crisis due to the growth of e-commerce. Since its March lows, MLT’s share price has since rebounded and hit an all-time high of S$2.13.

Based on its FY19/20 DPU of 8.142 cents, MLT’s current yield is at 3.82%. While MLT is a high-quality REIT to own, dividend investors may prefer to seek a higher yield before they invest.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »