Incorporated in 1964, Heineken Malaysia Berhad is one of two licensed breweries in Malaysia. Presently, it operates from a brewery situated along the Federal Highway at Petaling Jaya, Selangor. As of 5 August 2019, Heineken Malaysia is worth a total of RM6.9 billion in market capitalisation.

I recently went through its latest 2018 annual report 2018 and will give an update of its latest results, long-term business performance, and stock valuation.

Here are eight things to know about Heineken Malaysia before you invest:

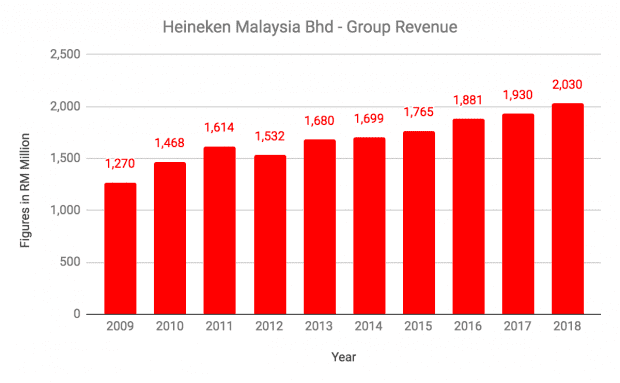

1. Heineken Malaysia has achieved a compound annual growth rate (CAGR) of 5.35% in group revenues, from RM1.27 billion in 2009 to RM2.03 billion in 2018. This is attributable to a consistent growth in domestic sales volume for its beverage products during the period. In 2018, domestic sales accounted for 99% of total sales.

(Note: Prior to 2016, Heineken Malaysia’s financial year ended on 30 June. This was moved to 31 December from FY2016 onwards. As such, I’ve adjusted the company’s revenue and earnings figures to reflect a financial yearend of 31 December.)

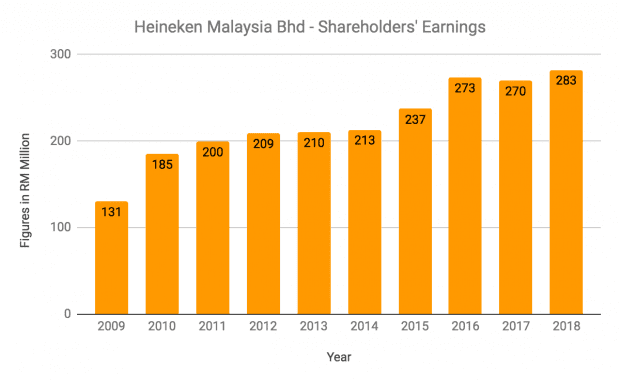

2. Heineken Malaysia has achieved a CAGR of 8.91% in shareholders’ earnings, from RM131 million in 2009 to RM282.5 million in 2018. Since 2010, however, earnings have grown at a CAGR of 5.40% which is remarkably similar to the company’s revenue growth rate.

3. Heineken Malaysia has a total of 12 brands in its beverage portfolio. They include:

| Beverage | Brands |

|---|---|

| Beer | Heineken, Anchor, Anchor Smooth, Anchor Smooth Draught, Tiger Beer, Tiger Radler, Tiger White, Paulaner, and Kirin Ichiban. |

| Stout | Guinness, Guinness Bright |

| Cider | Strongbow Apple Cider and Apple Fox Cider |

| Irish Ale | Kilkenny |

| Shandy | Anglia |

| Pre-Mixed Cocktail | Smirnoff Ice |

| Non-Alcoholic | Malta |

Source: Heineken Malaysia

4. As of 31 December 2018, Heineken Malaysia has no long-term borrowings and RM105.0 million in trade financing (short-term borrowings). The company also has current assets of RM604.2 million and current liabilities of RM535.6 million, giving it a current ratio of 1.13.

5. Heineken Malaysia’s cash conversion cycle (CCC) is only 2.5 days. It takes the company:

- 24.0 days to sell its inventory upon receiving it from suppliers

- 88.5 days to collect money from customers after billing them

- 110.0 days to pay its suppliers after being billed by them

Therefore, its CCC = Inventory Days + Debtor Days – Creditor Days = 24.0 days + 88.5 days – 110.0 days = 2.5 days

This shows why Heineken Malaysia doesn’t need to hold high amounts of cash to finance its business operations.

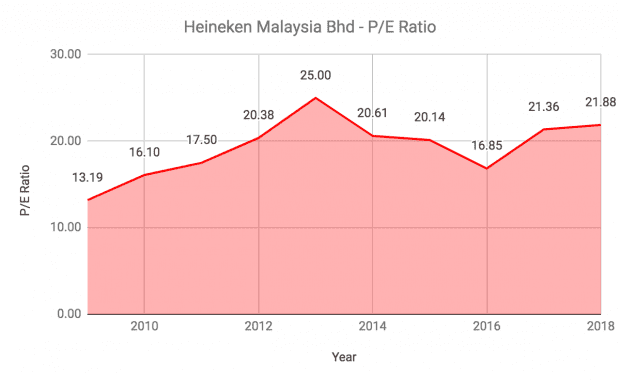

6. P/E ratio: Heineken Malaysia reported earnings per share of RM0.935 in 2018. Based on a share price of RM22.70 (as of 5 August 2019), Heineken Malaysia’s current P/E ratio is 24.28, which is above its 10-year average of 19.30.

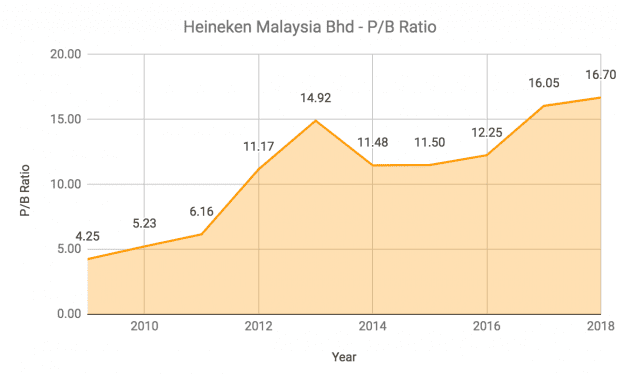

7. P/B ratio: As of 31 December 2018, Heineken Malaysia has net assets per share of RM1.23. Thus, it’s current P/B ratio is 18.46, which is above its 10-year average of 10.97.

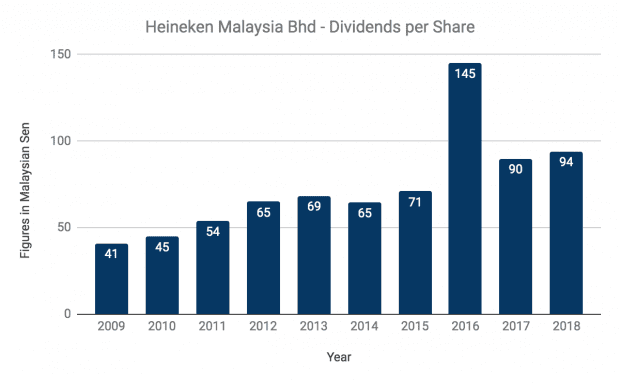

8. Dividend yield: Heineken Malaysia has consistently grown its dividends per share over the last 10 years, from 41.0 sen in 2009 to 94.0 sen in 2018.

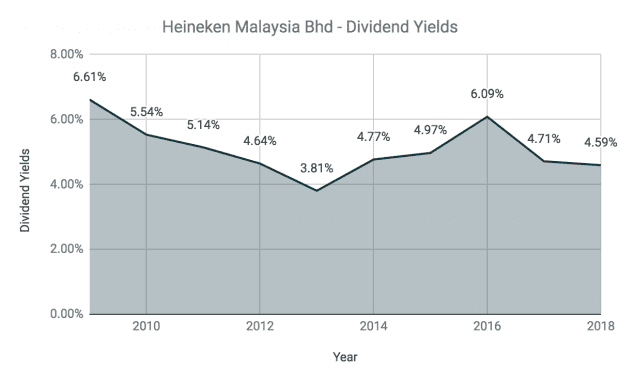

Based on its current share price, its dividend yield is 4.14%, which is below its 10-year average of 5.09%.

The fifth perspective

Overall, Heineken Malaysia has delivered steady growth in revenue, profits, and dividends over the past 10 years. However, a run-up in share price since October 2018 has seen Heineken Malaysia’s valuation climb even higher.

When compared to Carlsberg Brewery Malaysia, Heineken Malaysia’s stock valuations are also similar to its rival:

| Heineken Malaysia | Carlsberg Malaysia | |

|---|---|---|

| Share price (5 August 2019) | RM24.10 | RM23.86 |

| 10-year average P/E ratio | 19.30 | 18.27 |

| Current P/E ratio | 24.28 | 26.28 |

| 10-year average dividend yield | 5.09% | 4.63% |

| Current dividend yield | 4.14% | 3.27% |

While Heineken Malaysia is marginally cheaper than its rival, both companies are still trading way above their 10-year P/E averages. In the meantime, value investors may want to wait for a lower valuation before considering the stock.