Listed in 1969, Hong Leong Financial Group Berhad (HLFG) has established itself as one of the largest integrated financial conglomerates in Malaysia. It has three main businesses: banking, insurance, and wealth management services. As at 2 April 2019, HLFG is worth RM21.8 billion in market capitalization . It is among the 30 largest corporations listed on Bursa Malaysia and a constituent of the Bursa Malaysia KLCI Index.

In this article, I’ll bring a detailed account of HLFG’s track record over the last 10 years, and provide an update on its latest financial results and valuation.

Here are 10 things to know about Hong Leong Financial Group before you invest:

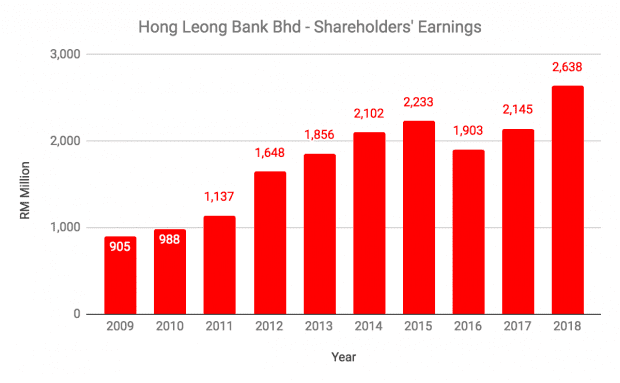

1. HLFG derives around 89% of its profits before taxation (PBT) from Hong Leong Bank (HBB), a 64.37%-owned subsidiary and one of the leading banking groups in Malaysia. Over the last 10 years, HBB has grown earnings at a compound annual growth rate (CAGR) of 12.6%, from RM905.3 million in 2009 to RM2.64 billion in 2018. This is mainly due to the growth in HBB’s net interest income, fee-based income, and net profits earned from Bank of Chengdu, an 18%-owned associate bank of HBB.

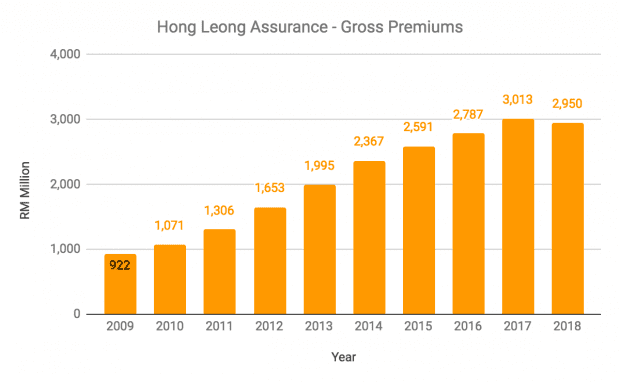

2. HLFG derives about 9% of its PBT from insurers Hong Leong Assurance (HLA) and MSIG Insurance (Malaysia) Berhad. HLFG owns 70% of HLA, the largest local life insurer in Malaysia. Over the last 10 years, gross premiums increased by a CAGR of 13.8%, from RM922 million in 2009 to RM2.95 billion in 2018. This is mainly due to its agency network which contributed double-digit growth in sales of investment-linked policies, and a strong partnership with HBB which contributed to growth in bancassurance sales during the period.

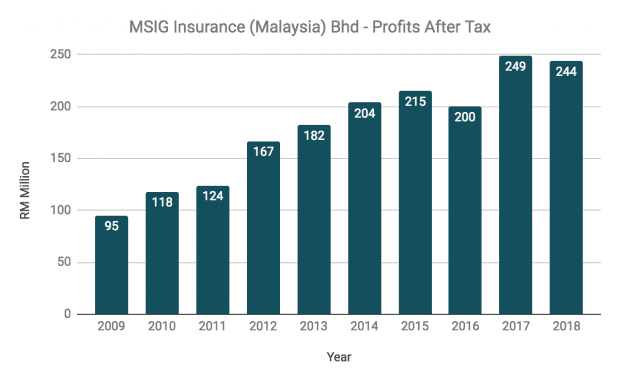

3. HLFG also owns 30% of MSIG, a leading general insurer in Malaysia. Over the past 10 years, MSIG grew its profits after tax (PAT) by a CAGR of 11.1%, from RM95.2 million in 2009 to RM243.8 million in 2018. This is mainly due to growth in gross premiums, income from investments, and steady underwriting margins from having a stable claims ratio over the last 10 years.

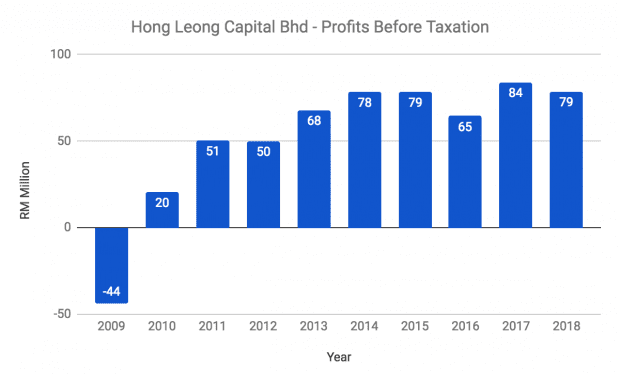

4. HLFG derives 2% of its PBT from Hong Leong Capital Bhd (HLCB), a 81.33%-owned subsidiary. The company provides a wide range of investment banking services such as stockbroking, futures broking, and unit trust management services. Over the last six years, HLCB averaged RM75 million in PBT, providing HLFG with a relatively stable source of income during the period.

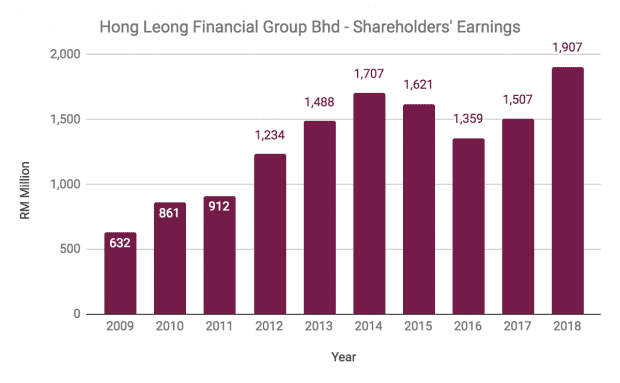

5. Overall, HLFG grew its revenue at a CAGR of 10.0%, from RM2.27 billion in 2009 to RM5.35 billion in 2018. This is mainly driven by growth from HBB and HLA. The conglomerate has maintained a cost-to-income ratio of 40-50% and a net profit margin at 30-35% for most of the 10-year period. Likewise, shareholders’ earnings grew by a CAGR of 13.1%, from RM632.0 million in 2009 to RM1.91 billion in 2018. HLFG saw a dip in earnings in 2016 due to a one-off mutual separation scheme expenses of RM172 million and lower profits from Bank of Chengdu that year.

6. Over the latest 12 months, HLFG generated RM1.94 billion in earnings and RM1.70 in earnings per share (EPS):

| Q3 2018 | Q4 2018 | Q1 2019 | Q2 2019 | Trailing 12 Months | |

|---|---|---|---|---|---|

| Earnings (RM millions) | 502.6 | 454.3 | 505.7 | 481.5 | 1,944.1 |

| EPS (RM) | 0.439 | 0.397 | 0.442 | 0.421 | 1.70 |

Source: HLFG quarterly reports

7. As at 31 December 2018, HBB had gross loans and financing assets of RM131.63 billion. Its gross loan impaired ratio was kept low at 0.8%. Total capital ratio was 16.6% and loan impairment coverage ratio was 122%. HBB has maintained a position of capital strength and is well capable of weathering a downturn in the future

Valuation

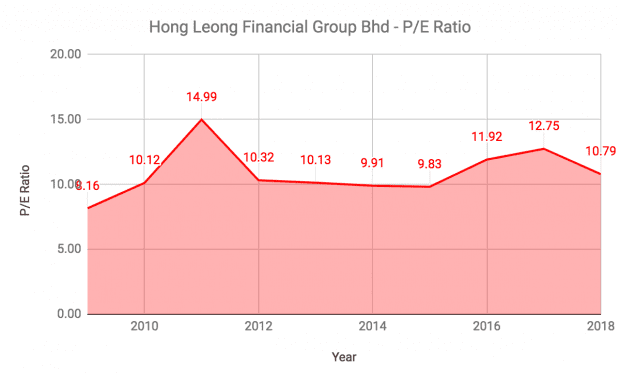

8. P/E ratio: As at 2 April 2019, HLFG is trading at RM18.98 a share. The group generated RM1.70 in EPS over the last 12 months. Therefore, its current P/E ratio is 11.16, which is marginally higher than its 10-year average of 10.89.

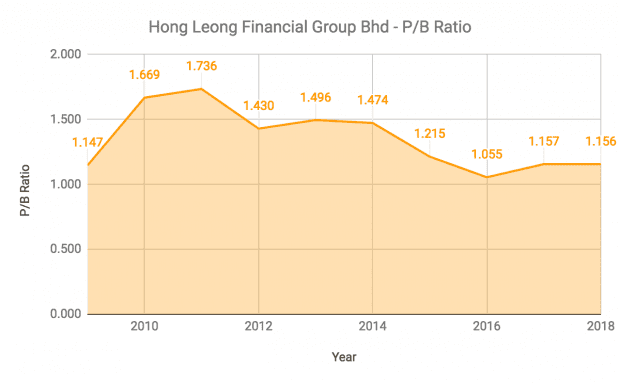

9. P/B ratio: As at 31 December 2018, HLFG reported net assets per share of RM16.21. Therefore, its current P/B ratio is 1.17, which is lower than its 10-year average of 1.35.

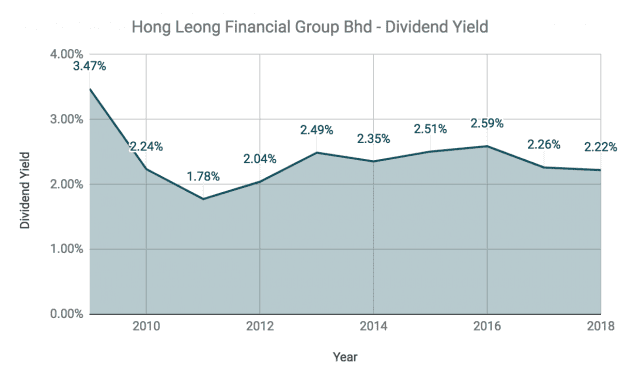

10. Dividend yield: In FY2018,HLFG paid RM0.40 in dividends per share. If HLFG maintains its dividend, its dividend yield is 2.11%, lower than its 10-year average of 2.40%.

The fifth perspective

Since HLFG derives almost 90% of its PBT from HBB, would it make sense to just invest directly in HBB? Let’s do a quick comparison of HLFG and HBB’s valuations:

| Hong Leong Financial Group | Hong Leong Bank | |

|---|---|---|

| Trailing 12 months earnings | RM1.94 billion | RM2.71 billion |

| Trailing 12 months EPS | RM1.70 | RM1.32 |

| Share price (as at 2 April 2019) | RM18.98 | RM20.06 |

| P/E ratio | 11.16 | 15.19 |

| P/B ratio | 1.17 | 1.68 |

| Dividend yield | 2.04% | 2.39% |

At current prices, HBB pays a better yield. But if you’re looking for yield, there are other bank stocks in Malaysia (like Maybank and Public Bank) that pay a higher yield. However, if you’re looking to own a piece of HBB, investing via HLFG looks cheaper based on their respective P/E and P/B ratios.