Block-what? If you’ve been following the news, there has been increased talk of more and more financial institutions – especially the big banks experimenting with and even implementing “Blockchain” technology in their operations.

UBS led a consortium of banks including BNY Mellon, Deutsche Bank and Santander to develop a “Utility Settlement Coin” which is a digital cash equivalent of major currencies backed by central banks. Goldman Sachs, JP Morgan, Morgan Stanley, Citi, Visa, NASDAQ and numerous others are also looking into it.

Locally, Singapore seems to be leading the pack in terms of institutions experimenting with this technology. Hitachi and Bank of Tokyo-Mitsubishi have started testing just last month. IDA, DBS Bank and Standard Chartered have also started developing blockchain-based technology for trade finance; Bank of America, HSBC and IDA have jointly developed Letter of Credit (LoC) transaction system based off blockchain technology; IBM in collaboration with the Monetary Authority of Singapore (MAS) and Economic Development Board (EDB) opened a blockchain innovation center in Singapore to accelerate adoption of blockchain.

Slated to possibly overtake London as the next major financial center, financial services is one of the larger economic pillars of Singapore. Not resting on its laurels and representing MAS at a keynote address at the Global Technology Law Conference, Ravi Menon mentioned drones, automation, digital payment services, deep learning and blockchain as the future. MAS isn’t the only central bank looking at blockchain, central banks all over the world are looking into this technology. So this is a pretty important technology, but what in Harambe’s good name (may he rest in peace) is Blockchain?

What is Blockchain?

You’ve probably heard of Bitcoin, the cryptocurrency born after the financial crisis when people and regulators lost trust in banks with their money. It’s one very controversial topic but we’re not headed there. Blockchain is what makes Bitcoin works, it’s the underlying technology that facilitates seamless transactions between parties.

Blockchain is not new technology

It’s not a new technology, it’s based on numerous existing technologies blended together – distributed systems, hashing functions, p2p networks, public-private key cryptography and cryptographic signatures. These can be highly technical and complex but I’ll use publicly available pictures to portray what they are. For further technical explanation, I’ll leave it up to the reader to research more on each function.

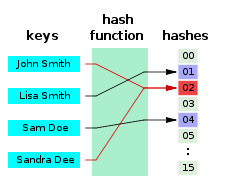

Hashing Functions:

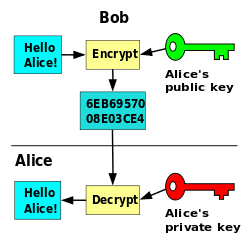

Key Cryptography & Cryptographic Signatures:

Distribution systems and P2P networks are essentially the same thing and will be explained further below.

Blockchains can’t be altered

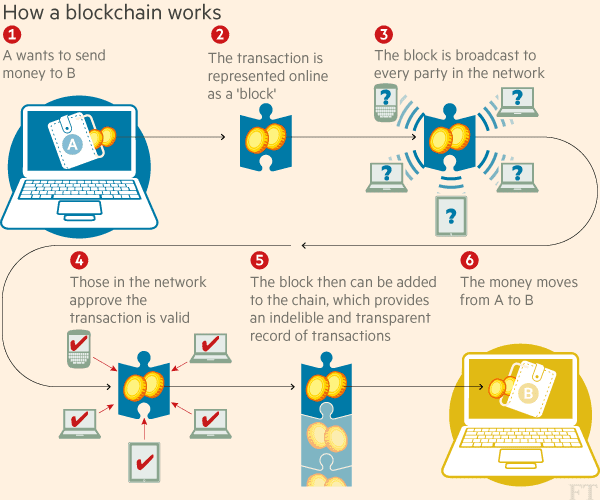

Blockchain can be thought of as a ledger – recording transactions, which are time-based and can’t be altered. Endless cases of financial fraud or risky outsized bets happen at financial institutions and it may sometimes take months if not years to discover them; some can even be hidden until today because they can be changed or deleted without trace. Blockchain records ALL transactions in electronically indelible ink, and the transaction will stay there for the rest of time.

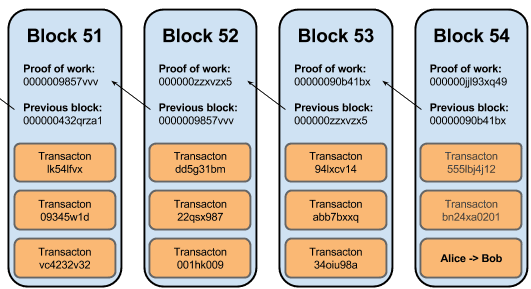

Think of Blockchain in a literal way – it’s a bunch of blocks that are strung together by a chain. Each block is numbered in ascending order starting with zero, the number is the “height” of the block.

A block only directly links to the one preceding it, all data stored within the block is read-only and can’t be changed – making it tamper-proof. Each block represents a set of transactions (or events) that happened over a particular period.

Blocks aren’t identified by its height but by its unique identification (ID), each ID is the hash of the data within that block. An example: Block 0=00000002398fn2873h28fn28b3b249. This is the Block’s ID, and it’s the digital fingerprint of that particular block.

Each block stores data. In Bitcoin, the data would be transactions, but the wider application of blockchain means that the data could be anything from transactions to contracts; any digital data.

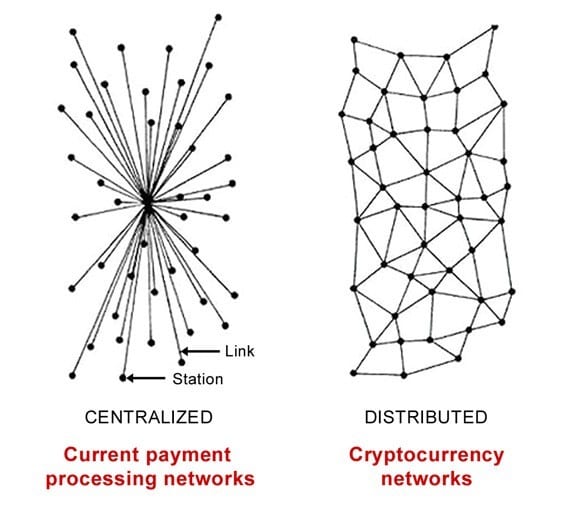

Decentralized network

Blockchain runs on multiple, equal nodes with multiple connections to other nodes, like a web. This makes the system highly resilient to attacks. See below for an illustration of how it looks like:

Most if not all transaction-based businesses like Visa or Mastercard run on a centralized system, this means that if the data center gets hit with a power outage, the entire system goes dark. Blockchain’s distributed ledger architecture is radically different as every computer is essentially a node and data is distributed to all nodes. If a single node goes down, the other nodes will still be running and data will never be lost. This makes hacking the Blockchain immensely difficult as a hacker has to take down every single node to destroy the entire system. This architecture also gives easy access to every block and node in the network.

When Lehman Brothers went bust, it took years to untangle all the open trades and figure out where the assets were – a costly and tiresome process for all involved. On a blockchain-enabled system such a failure would not lead to catastrophic uncertainty because there would be no open trades. With a distributed ledger, everyone knows the exact location of all assets at all times.

Advantages of Blockchain

1. Trust

Blockchain’s real innovation isn’t really the tamper-proof, distributed network system, but the underlying emotional raison d’etre during its birth powering the Bitcoin: a trustless system.

The financial crisis wrecked trust in financial institutions and recent capital market shenanigans brought on by endless central bank interventions have further eroded trust in the overall system itself. Banks exist because people can’t be trusted to deal honestly with money, the very root of banking is trust. If we humans were completely honest, banks wouldn’t exist.

Banks are trusted to keep our money safe and confidential, sending us regular records of how much money we have and is a trusted means to send and receive money from each other to ensure that people don’t cheat us.

Most of us if asked where our money is, we would instantly say “in the bank”. It’s a partially right answer in that a record of our money is kept in the database of the bank. If we want to do anything with our money, we must first send an instructional order to that particular bank.

In the Blockchain world, our money is an entry in a single ledger but copies of it being spread on countless computers connected in a vast network – it’s everywhere and nowhere at the same time. Our records are secured with a cryptographic key only we know; in essence, we can say that our money belongs to us, and not at some bank – a more comforting thought.

2. Uses

It isn’t just financial transactions that Blockchain can be utilized, a couple in Singapore effected a prenuptial agreement onto a Blockchain (prenups aren’t legally enforceable in Singapore, sorry) – that is a smart contract.

By adding programming capabilities to the Blockchain ledger, more complex contracts can be made. Most financial transactions are highly complex but let’s take a simple escrow arrangement as an example:

Escrow arrangements where funds are only transferred when goods are delivered is one of the most common financial transactions in almost everything we do. Since everything on a Blockchain has a unique ID – they can send and receive information – they can hold money and be programmed to make autonomous decisions about buying and selling things.

If a firm’s customers are on the Blockchain, it would be able to check their creditworthiness (without compromising their privacy). It would also be easier to arrange for direct, immediate payments via the Blockchain. This reduces costs for intermediaries like credit card companies and traditional transfer of funds that can take days or weeks can be reduced to seconds.

“Imagine a global financial infrastructure that is slim, trim, safe and secure. A system that combines the ease and finality of cash payments with the speed and reach of global communications. Where transaction fees are reduced to the minimum, because the effort to carry out transactions is minimal as well. A system so robust that it could easily survive the collapse of even the largest institution, making too-big-to-fail a thing of the past. A world where stocks and bonds administer themselves: automatically paying dividends and coupons, registering their new owners, and reporting on their prices.” – UBS

3. Transaction costs

The action of swiping your credit card for pumpkin spice latte at Starbucks may seem stupidly simple but the transaction is highly complex as the data passes through countless intermediaries and takes days to clear. Further, it’s at risk of glitches and fraud – what if one of the parties suddenly go bankrupt?

Blockchain eliminates all this through real-time settlement, drastically reducing counterparty risk and the need to post expensive collateral at central banks to insure it. This frees up capital for corporations, banks and investors.

Think about our trading/investing activities – when a trade is made, the money is tied up until it’s settled. Under Blockchain, funds will be ready immediately.

4. Cryptocurrencies

Like Bitcoin, there’s DogeCoin and many other cryptocurrencies out there. As mentioned above, UBS’s Utility Settlement Coin is just a fancy term for a cryptocurrency. It’s backed by hard currencies like the US dollar and the Euro. Cryptocurrencies can be backed by anything – hard currencies, gold, anything.

A vast majority of people are still cynical about cryptocurrencies but we use them in our daily lives without even noticing it: loyalty points at Capitaland, Krisflyer Miles at Singapore Airlines, gift certificates for Takashimaya. Cryptocurrencies are no different. Frequent flyer miles are in essence an agreed medium of exchange – the same as money. You trust Singapore Airlines to honor your Krisflyer Miles without even thinking twice about it.

5. Physical assets

Your house is an asset that you own, and your ownership is recorded by a network of intermediaries. But a corrupt government can sometimes erase their ledger and demand that you give them back the land that you rightfully own. Other assets such as your laptop, jewelry or phone has proof of your ownership in terms of a sales receipt, once you lose it, it’s hard to prove ownership.

Physical assets can have the same unique ID the same way people do and can be accounted for in a Blockchain. Instead of representing money, the blocks represent tokens of physical assets.

If Blockchain made it possible to build a tamper-proof and fully-automated system for maintaining a ledger of transactions, what other kinds of financial transactions or smart contracts could it potentially keep track of? Moreover, Blockchain has the potential to radically reduce business administration costs by automating such things as payroll, accounting, VAT payments and regulatory compliance. And if the blockchain enabled automatic bitcoin transactions that were immediate and final, what other kinds of transactions could it theoretically automate? It’s potentially limitless.

6. Reduce fraud

Fraud can be reduced as regulators can program compliance rules directly into the Blockchain, and the system is automated to check transactions against the list of criminals, sanctions, terrorism and block potential fraudulent transactions.

Roadblocks for the Blockchain

This technology is still very new and unknown to most, trust in its application is nowhere near the trust we give our banks. Powerful incumbents or governments may try to stop this technology as it can create an entire sub-economy that can’t be tracked should the owners of the Blockchain choose not to reveal the underlying transactions.

There’s currently no legal framework for Blockchain as it’s so new and its applications seemingly limitless. How do you legally recognize both a complex billion-dollar M&A transaction and a prenuptial agreement?

Blockchain is 100% digital, and if you know a little thing or two about Bitcoin, you’ve heard of Bitcoin mining. As more and more blocks are added to the chain (with none being erased), more and more data and power will be consumed to support the network. Will this be sustainable for large players using this technology? Imagine the millions of transactions Visa handles on a daily basis, and transpose that to a Blockchain where every single transaction is a new block.

The Fifth’s perspective

It’s a game-changing technology that could disrupt industries but it will take years before we see it come to fruition – as investors, we should be aware of any new technology on the horizon that have wide-ranging disruptive capabilities to prepare our portfolios, financial well-being and job security. This is just one of the many possible tech out there that may affect everything we know for better or for worse.

if it’s so secure and every node has a record of the transaction, why can 480,000 coins disappear into thin air? surely the records of these coins still exist?

Interesting. Do you have a link/source on that?

i am not good at adding links, but you can for example check wikipedia and mt.gox.