Established in 1979, Kossan Rubber Industries Berhad is presently one of the three largest rubber glove manufacturers in the world. As of 26 August 2019, Kossan is worth RM5.3 billion in market capitalisation.

In this article, I’ll give an overview of the company’s growth story, long-term financial results, and stock valuation. Here are 10 things to know about Kossan before you invest:

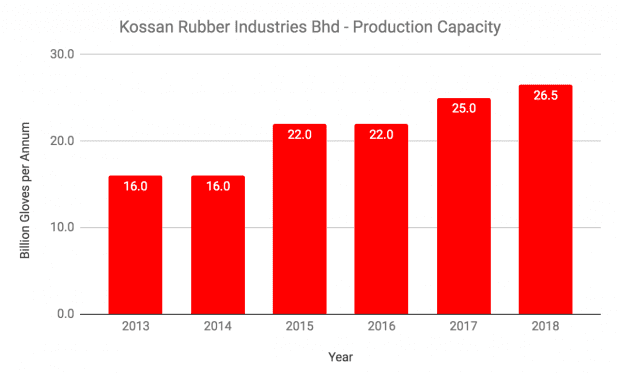

1. Annual production capacity has steadily increased from 16.0 billion gloves in 2013 to 26.5 billion gloves in 2018.

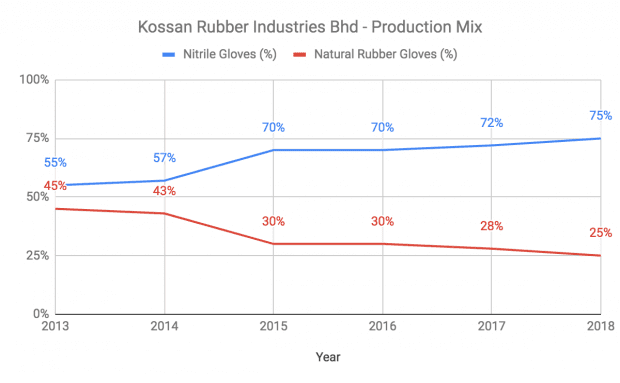

Kossan’s production mix has skewed heavier towards nitrile gloves over natural rubber gloves as the new plants are constructed to produce the former. Nitrile gloves now comprise 75% of production. Kossan exports its products to over 180 countries but the U.S., the eurozone, and ASEAN account for the majority of exports.

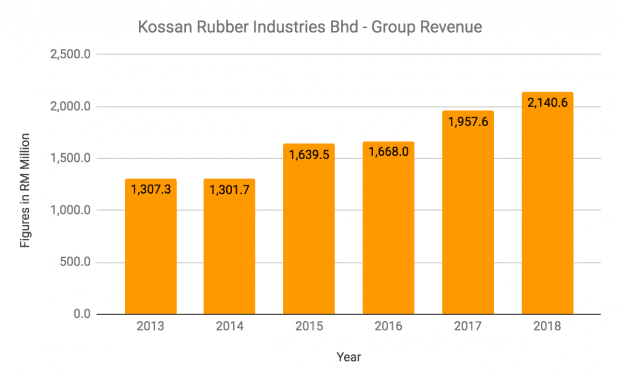

2. Revenue has grown at a compound annual growth rate (CAGR) of 10.37% from RM1.31 billion in 2013 to RM2.14 billion in 2018.

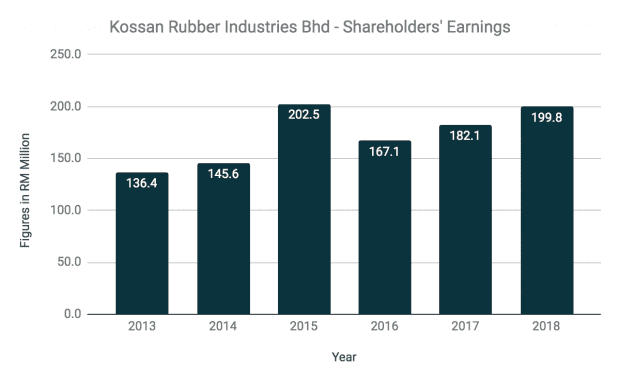

Shareholders’ earnings has grown at a CAGR of 7.93% from RM136.4 million in 2013 to RM199.8 million in 2018. Over the last five years, Kossan’s average return on equity is 17.26%.

3. From 2014 to 2018, Kossan generated RM1.00 billion in cash flows from operations and raised RM274.4 million in net long-term debt. Out of which, it has spent RM952.7 million in capital expenditures and paid RM294.2 million in dividends to shareholders. As of 31 March 2019, Kossan has RM317.5 million in non-current liabilities and RM1.36 billion in total equity, and therefore a gearing ratio of 23.3%. It also has current assets of RM853.2 million and current liabilities of RM489.2 million, and a current ratio of 1.74.

4. In December 2018, Kossan received U.S. FDA 510(k) approval for its fentanyl-resistant nitrile gloves. Its development is in response to fentanyl drug abuse which has become a major concern in the U.S. This follows the company’s research and development of Low Derma™ gloves in September 2016 and Confidenz™ Halal-certified gloves in November 2017.

5. In November 2018, Kossan opened Plant 17 which has an annual production capacity of 1.5 billion nitrile gloves. The company has also begun construction for two more new plants: Plant 18, which has an annual production capacity of 2.5 billion gloves, is scheduled for completion in Q3 2019; and Plant 19, which has an annual production capacity of 3.0 billion gloves, is scheduled for completion in Q4 2019.

6. In March 2018, Kossan completed the acquisition of two pieces of leasehold land — measuring a total of 824 acres — in Bidor, Perak for RM82.4 million. The land purchase is intended to be used for the company’s next phase of expansion. Kossan plans to start development at Bidor in 2020 and expects the project to be fully completed within eight years.

7. As of 15 March 2019, Kossan’s five largest shareholders and their direct shareholdings are as follows:

| Substantial Shareholders | Direct Shareholding |

|---|---|

| Kossan Holdings (M) Sdn Bhd | 51.06% |

| Employees Provident Fund Board | 7.70% |

| Kumpulan Wang Persaraan (Diperbadankan) | 2.20% |

| Public Ittikal Sequel Fund | 1.60% |

| Tian Senn Resources Sdn Bhd | 1.56% |

Founder and CEO, Tan Sri Dato’ Lim Kuang Sia, along with his brother, Lim Leng Bung, are executive directors and the largest shareholders through their stakes in Kossan Holdings (M) Sdn Bhd. Tan Sri Lim’s son, Lim Ooi Chow, and nephews, Lim Siau Tian and Lim Siau Hing, are all executive directors as well. The Lim family remains firmly in control of the company as they occupy five out of nine seats on the company’s board.

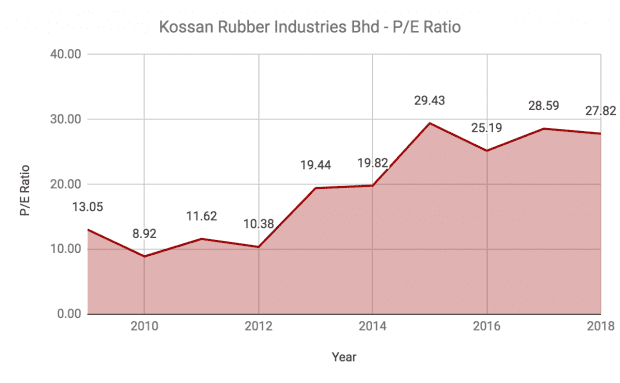

8. P/E ratio: Kossan posted earnings per share (EPS) of RM0.156 in 2018. Based on the company’s share price of RM4.18 (as at 26 August 2019), its P/E ratio is 26.79, close to its five-year average of 26.17. However, from the chart below, you’ll notice that Kossan’s P/E ratio has expanded sharply in the last four years as its share price has risen faster than earnings growth. If you take into account its historical range over the last 10 years, Kossan’s average P/E is closer to 19.43.

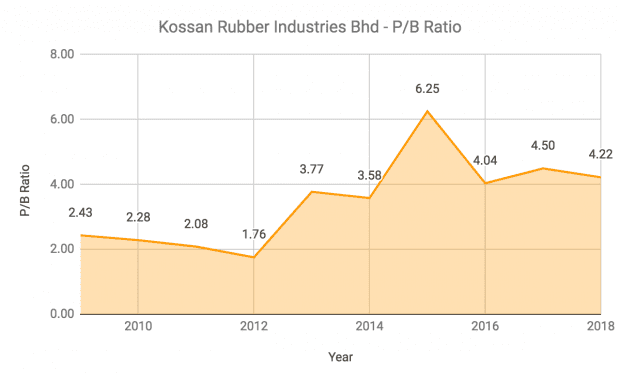

9. P/B ratio: As of 31 March 2019, Kossan has RM1.03 in net assets per share. Thus, its current P/B ratio is 4.06, which is below its five-year average of 4.52.

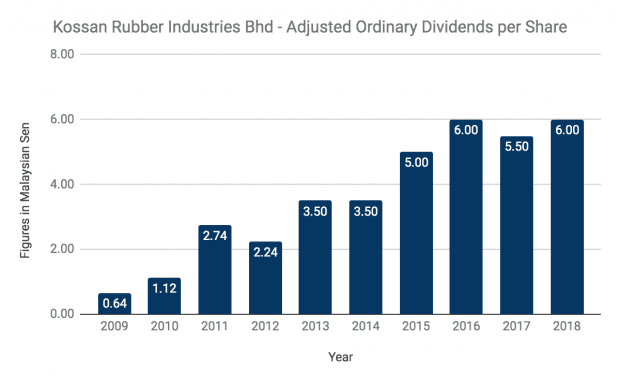

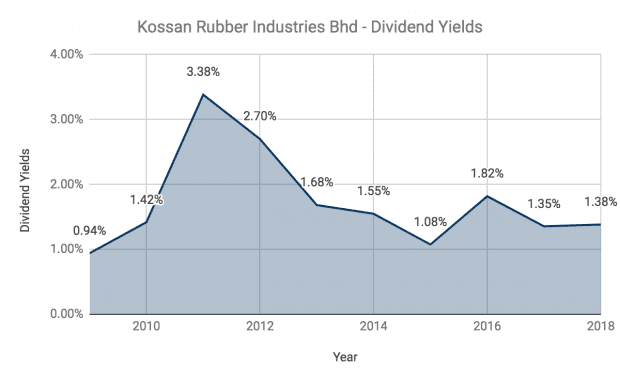

10. Dividend yield: Kossan paid a total dividend per share (DPS) of 6.0 sen in 2018 – a tenfold increase from 0.6 sen in 2009.

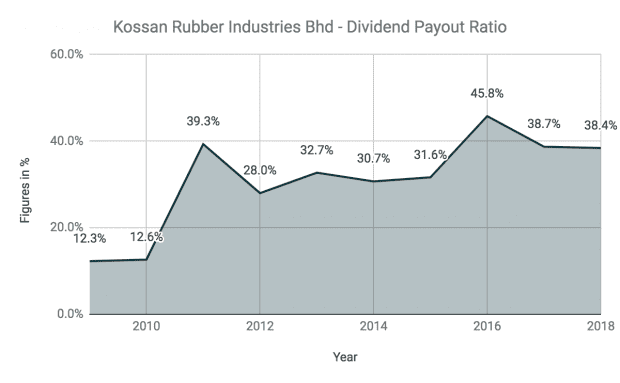

Over the same period, the company’s EPS has only grown threefold. The main reason for the higher DPS growth is because the company increased its dividend payout ratio from 12.3% in 2009 to 38.4% in 2018.

Assuming Kossan maintains its DPS, its current dividend yield is 1.44%, which is exactly its five-year average.

The fifth perspective

Kossan Rubber Industries has delivered steady growth in revenue and earnings over the last 10 years. The rubber glove industry looks set to continue growing based on rising awareness about hygiene and infection control, and demand is projected to reach 300 billion gloves in 2019.

At the same time, the rubber glove industry is a competitive one with larger players like Top Glove and Hartalega competing with Kossan for market share.