There are countless models you can use to calculate the amount of money you need to retire comfortably in your golden years. But if you’ve ever been overwhelmed by the many different methods out there and the complex calculations used, not to worry because there’s one quick and simple way to estimate how much you need for retirement: the rule of 300.

Simple take the average amount you spend every month and multiply by 300. That’s it!

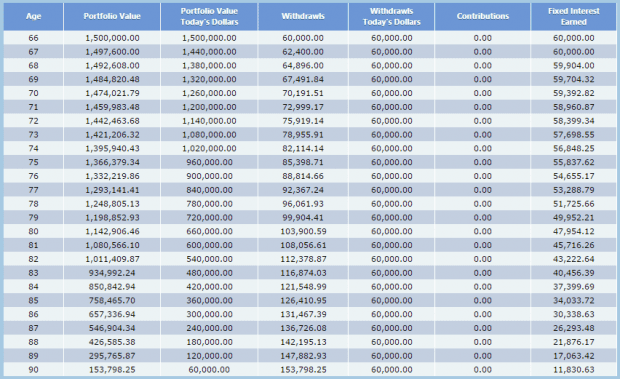

So if your average monthly household expenditure is $5,000, then you need $1.5 million to retire (5,000 x 300) and that amount should last you for the next 25 years. So if you retire at 65, your retirement fund will last you till 90 — which is a pretty nice time to go.

How does the rule of 300 work?

As finance blog, Johnny Moneyseed, pointed out, the rule of 300 is based on the 4% rule in retirement. The 4% rule refers to your withdrawal rate: the annual percentage amount you withdraw from your investment portfolio when you retire.

So if you have $1.5 million in your portfolio, you withdraw 4% a year to use in your retirement.

So in your first year, you withdraw:

$1.5 million x 4% = $60,000

Which works out to exactly $5,000 a month for you to spend.

What about inflation?

Yes, we all know that the price of goods and services rise in price over the years, so you need to factor inflation into your withdrawal rate every following year as well.

So if inflation in growing at, let’s say, 4% a year, then your second year’s withdrawal amount is $62,400 (60,000 x 104%). Your third year’s withdrawal amount is $ 64,896 (62,400 x 104%) and so on and so forth.

So the question now is: how does the rule of 300 and the 4% withdrawal rate keep up with the pace of inflation?

Simple. It assumes that your portfolio also grows in value every year – at least 4% p.a. as well, in fact. So if your portfolio grows by 4% a year, inflation is at 4% a year, and you withdraw 4% of your portfolio for spending every year, theoretically, the rule of 300 of will last you comfortably for 25 years before your funds are all withdrawn.

Source: Four Percent Rule

Of course, if our portfolio grows by more than 4% a year, then your funds will last longer than 25 years. And if you’ve been reading this site for some time, you know that getting anything above 4% p.a. is very achievable; REITs alone give you a consistent 5-8% yield per annum (even higher if you buy at the right time!). Take a look at our S-REIT data table to see what we mean.

Disadvantages of the rule of 300 and the 4% rule

The 4% rule was first mentioned when a paper, Retirement Savings: Choosing a Withdrawal Rate that is Sustainable by Philip L. Cooley, Carl M. Hubbard and Daniel T. Walz, was published in 1998. Since then, the 4% withdrawal rate has been used as a rule of thumb for retirement planning.

The 4% rule and the rule of 300 is easy to use but, of course, when any model is that simple and straightforward, it can’t take into account every possible scenario that might occur in your retirement. For example:

- Market fluctuations. The market doesn’t give steady returns year after year and fluctuates up and down most of the time. Of course, if you invest in more stable assets like large-cap dividend stocks, REITs, and bonds, you’re more likely to generate steady returns every year compared to an investor who hunts for growth and quick capital gains.

- Market crashes. Sometimes, the market collapses (like in 2008-2009) and the value of your portfolio will drop substantially. Do you still withdraw your entire 4% then? On the other hand, a market recession is usually the best time to purchase great stocks at bargain prices that will drastically increase your returns and yield once the market recovers.

- Lifestyle changes. Even from 65 to 90 onwards, you can’t assume you’ll be living exactly the same lifestyle you live now which requires the same amount of expenditure every month. Your tastes and preferences will change over time and you might find yourself buying that red sports car you never got to drive when you were young, virile and had no wife to nag you about buying that red sports car. Well, it’s never too late, but if you plan on spending more, you have to adjust your finances accordingly.

- Health costs. And of course, the biggest worry and financial stress we all face in old age is the cost of medical care if we fall ill. Doctors and hospitals are expensive and if you’re not properly insured in your old age, your assets could be wiped away after a few years of pricey medical treatment. So make sure you are fully covered by insurance early!

The fifth perspective

The rule of 300 is a great way to find out how much you need for retirement quick and easy. If you have no idea at all what you need for retirement, you can use the rule of 300 right now to quickly find out how far away (or near) you are from your retirement goals.

At the same time, you probably want to factor in additional possible scenarios (medical care, market recessions, etc.) just to make sure you’re on the safe side. While it’s great to have too much money at the end of your life, nobody wants to have too much life at the end of money! So use the rule of 300 as a simple rule of thumb to get yourself started on your retirement needs and work from there!

After reading the article to understand the calculation, i find that it should be emphasized that the monthly expenses that is used to multiply by 300 is “inflation adjusted” current monthly expenses. Unless one is retiring this year, we can’t simply multiply the current monthly expenses by 300.

Otherwise, a 30 years old and 65 years old person would need the same amount of retirement fund, but both will run out of money at age 55 (30+25) and age 90 (65+25) respectively. The younger guy will have years of life ahead of him when the money ends…. Oouchh… 🙁

So for the 30-year old guy, the monthly expenses used to multiply by 300 must first be inflation adjusted until his desired retirement age. i.e. use current monthly expenses and compound it with inflation rate for 35 years (assuming the 30 year old guy will retire at age 65). Only after that, use the inflation adjusted monthly expenses to multiply by 300. Then the result will be the projected retirement fund needed at age 65. The Rule of 300 model could provide a general approximation but need to use the inflation adjusted monthly expenses, not the current monthly expenses.

Good sharing though, thanks for this article, i know another method 🙂 For those already in retirement, using current monthly expenses is correct. But remember that under this model, the money will run out in 25 years.

Hi HS,

Thanks for your comment!

At 30 years old, one probably wouldn’t be withdrawing from their retirement fund because I assume most people would still be working at that age to build their fund in the first place.

But you’re right on the point that a 30-year-old needs to use an inflation-adjusted figure for his monthly expenses and then multiply that by 300 to calculate his target for retirement.

So a 30-year-old who wishes to retire at 65 with $5,000/month would actually need $19,730/month in future dollars (at 4% inflation p.a). Multiply that by 300 and he would need at least $5,919,000 to retire.

If that sounds scary, it only goes to show how important investing is to retire comfortably!

Hi Adam, you are right, it is a big amount for retiremen but luckily it is a future value 🙂 Base on this model, retiring at age 65, the money çan last until age 90 (the rule of 300 model is assuming that the post retirement ROI is 4% p.a., inflation of 4% p.a., the retirement fund shall last 25 years at the withdrawal rate of 4% per year)

If we use a post retirement ROI of 6%, and plan the fund to last until age 80, that will reduce the required amount significantly. However, it is also important that during the pre-retirement stage, if one chooses to live within the mean or below what he could afford, the amount required for his retirement could be lower. Wants are limitless, but needs are limited.