Many of you reading this article would be aware that The Fifth Person has been following ARA Asset Management (ARA) very closely as we have a vested interest in the company since 2012.

I am writing this article since quite a few of you wanted to know whether we will be taking up the recent privatization offer made by a consortium led by founder John Lim.

The short answer is:

“No, we are voting against it.”

The Offer Price of S$1.78 is a price we think is not fair enough. Let me explain why.

In 2013, ARA was trading above S$1.80 and we could have sold it then for a handsome profit within a year. Obviously, we did not do that since we thought the market was not valuing the company adequately enough.

In 2011, ARA was managing around S$20 billion in assets under management (AUM). Today, the AUM has grown to S$30 billion as of 30 September 2016. Shareholders who invest in ARA would know that ARA is in the fund management business and the higher its AUM, the higher its revenues and profits are.

As much as AUM is important for the company and shareholders, ARA must continuously add value to its clients who entrust their money to ARA’s management. This value-add boils down to the performance of the fund. Since the company’s public listing in 2007, ARA has successfully divested a few private funds under their management and generated impressive double-digit returns for their clients.

Good performance will attract more money from new and existing clients and the AUM is likely to grow as long as ARA continues to achieve its targeted return.

So the question is: What is the value of a fund management company if it were up for sale?

I remember having this question answered by a fund manager who manages billions of dollars in assets. According to his observations, the value of the fund management company depends on the fund’s past performance.

If the fund’s past performance produced an average return, the fund is worth approximately 5% of its AUM. But if the fund met its targeted returns or higher, it can fetch a higher price at 7-8% of its AUM. Needless to say, if the fund is loss-making, it can only expect to be priced at less than 3% of AUM. This is an invaluable insight and comes in handy to solve our equation.

ARA’s fund performance has been terrific. With the offer price at S$1.78, the consortium is basically valuing ARA at 5.9% of its AUM. In my opinion, that figure is too low compared to the going market rate.

So, what can we do about it?

For us, we could simply take profit, happily move on, and find another idea. But for those who bought above S$1.78 in 2013, they are likely to feel disappointed. The opportunity cost is not a joke for them.

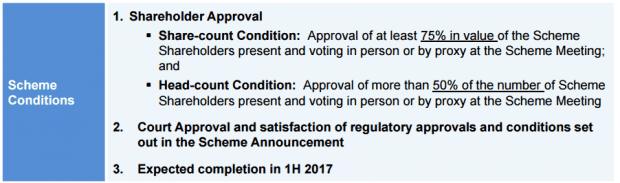

Now, minority shareholders usually think that they can’t do anything but ARA’s privatization offer (Scheme of Arrangement) is conditional upon two items.

Scheme of Arrangement. Source: ARA Asset Management

The Scheme of Arrangement requires 75% approval by shareholding. However, majority shareholders — Cheung Kong, Straits Trading, and John Lim, who together account 46.2% of total shares — will abstain from voting, which means minority shareholders will have a voice that’s twice louder than usual. The Scheme of Arrangement also requires the approval of at least 50% of the shareholders present at the meeting, regardless of shareholding. If more than half of the shareholders at the scheme meeting vote against the resolution, the deal is off.

I’ve heard of companies using their own employees (who are each given shares) to attend and vote for resolutions to ensure they get passed (though, in good faith, I highly doubt that ARA will do anything like that). On the flip side, I’m sure there are some minority shareholders who have also done the same by getting their friends and family to purchase one lot of shares in order to vote against a resolution they’re unhappy with. Of course, this tactic only works with a head-count vote — which is what ARA is using during the meeting.

On a side note, I’ve always found it enriching to attend ARA’s meetings. I have said this before — ARA is probably one of the few companies where minority shareholders should attend their annual meetings because there is a lot of things to learn from ARA’s capable and trustworthy board of directors. It was a rare sight in Singapore indeed when I witnessed directors Justin Chiu, John Lim, and Edmond Ip waiving their entitlement of director fees in AGM 2014.

ARA is one of a kind

I hate to say this but I (and we) will be voting against the privatization offer.

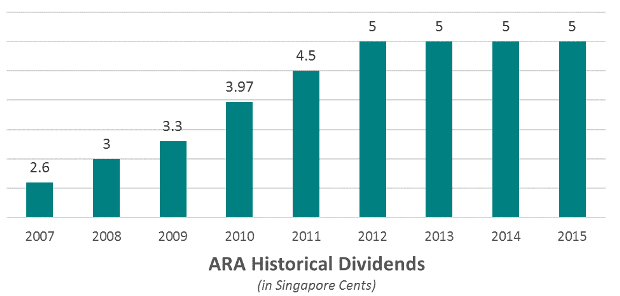

ARA is a one-of-a-kind company listed on the Singapore Exchange. ARA’s business model is special – the company manages real estate funds, but its revenues and profits don’t follow real estate cycles. ARA’s income is pegged to property valuation and net property income, which are relatively stable in nature. ARA’s historical dividends also give us a glimpse of the company’s resiliency. A remarkable business like this is very hard to come by and we certainly do not want to let it go at the wrong price.

Let me add one more plus point about ARA.

ARA is not your typical fund; they do not suffer from redemption issues.

During a market sell-down, a fund manager usually gets a lot of pressure from panicked clients who redeem their shares. This will cause the fund’s AUM to drop, thus lowering the income for the fund manager. However, this does not apply to ARA. Nearly three-quarters of ARA’s AUM is based on the property value of public-listed REITs. Unitholders who panic may offload their REIT shares during a crash thereby causing REIT prices to fall, but the underlying value of the REIT’s properties remain the same. So technically speaking, this doesn’t reduce ARA’s AUM.

For ARA’s private funds, ARA locks up its clients for a period of five to ten years. Should ARA perform well enough by the end of fund’s term, a new fund will be set up and new/existing clients can again invest their money into this new fund. Remember, this is an industry where people give you money because you can perform, not because you’re the cheapest. That’s the reason why, over the past five years, we see lucrative net profit margins (>50%) and return on equity (>15%) for ARA.

Perhaps the company which shares characteristics closest to ARA is Kenedix Group that’s listed in Japan. Like ARA, Kenedix manages a number of private funds and J-REITs. The company’s AUM stood at ¥1,644 billion as of Dec 2015. At the time of this writing, Kenedix is trading at a market capitalization of ¥116 billion. The market is implicitly valuing Kenedix at 7% of its AUM. Should ARA be valued at a similar percentage of AUM like Kenedix, ARA’s share price should trade at S$2.10.

You may or may not agree with this single valuation metric. As Mark Twain once said, “To a man with a hammer, everything looks like a nail.” But we do have other metrics indicating that ARA deserves a better valuation than the current offer price of S$1.78. Regardless, I think that percentage of AUM still best represents ARA’s underlying value — and S$1.78 is definitely not a price we will consider.

The fifth perspective

By doing this evaluation, we hope other minority shareholders of ARA can get a fuller picture of how much we should be fairly compensated. There is still a possibility that the deal will be called off and we will be more than happy to hold onto ARA’s shares for the long term and ride along its robust growth. Like the American private equity giant, ARA has the potential to be the Blackstone of Asia. And I, for one, hope to see ARA do well and reward its shareholders, who’ve loyally stuck with the company for years, accordingly.

Read more: Farewell, ARA… What I learned from my very last meeting with ARA Asset Management

If I was a major shareholder and I want to buy the remaining share from minor shareholders, would I want to buy it at a (bearish) cheap price or (bullish) expensive price.

Definitely at a cheap price.

If I were to follow your thinking of a 7% Price:AUM, with the recent blockbuster announcement of Century Link, AUM should be at 34 billion, ARA should be privatised at $2.3. Current privatization price is 30% discount from the the 7% P:AUM valuation.

At the same time, their incoming partners AVIC and Warburg Pincus seem to be able to provide a lot of value to the business, I would rather they come in and add value to me then I take $2.30, unless they offer me something much higher. This also supports the usual privatization thinking that it should command a premium over the “right” valuation.

Conclusion. The offer price is too cheap. I support fifthperson to vote against privatisation.

Good point, Weihan. If we were to take into account the newly set-up ARA Harmony VI with an AUM size of S$4 billion, then ARA’s value would have grown, even though ARA Dragon Fund 1 with an AUM size around S$1.6 billion is coming off a divestment this year.

You have any views on super group ?

Hi Harris,

Personally, I think the offer for Super Group is good and Jacobs Douwe Egberts paid more than fair value to acquire it.

I like your report onARA. Hope to get regular update of your reports thanks

Thanks, Phil! Glad you found it useful 🙂

Dear Rusmin:

THank you for sharing your views. I will be voting against too.

Do u think speaking with the big funds in a discussion to rally together will make a difference? By banding together, we can make a united request to the offerors.

If the big funds are aligned, then 25% against will not be difficult. That alone fails the delisting offer.

Matthews International Cap Mgmt LLc 102,488,519 10.28 -2,275,500 -2.17 1.10 10/31/2016

Franklin Advisers Inc 53,934,103 5.41 0 0 3.41 10/31/2016

Mawer Investment Management Ltd 23,492,235 2.35 0 0 1.18 09/30/2016

Prusik Investment Management LLP 19,143,716 1.91 0 0 2.28 07/31/2016

Jackson National Asset Management LLC 11,411,341 1.14 0 0 2.30 06/30/2016

Franklin Intl Small Cap Growth Adv 46,734,622 4.69 0 0 3.38 09/30/2016

Matthews Asian Growth & Inc Investor 36,838,667 3.70 0 0 1.32 06/30/2016

Matthews Asia Dividend Investor 34,749,418 3.49 0 0 0.77 06/30/2016

Matthews Asia Small Companies Inv 11,869,818 1.19 2.33 06/30/2016

JNL/Franklin Templeton Intl Sm Cap Gr B 11,411,341 1.14 0 0 2.30 06/30/2016

Transamerica International Sm Cp Val I 7,632,240 0.77 09/30/2016

Hi Contrarian,

Every fund has their own investment mandate and it is best they make their own decisions on what’s best for the interest of their clients. ARA’s focus on growing its private equity business may no longer suit the big funds’ (i.e. Matthews/Franklin) investment mandates and, thus, it may make more sense for them to liquidate their positions.

Im a shareholder and by selling at this price I make a gain.

What’s to prevent ARA to pay no dividends from now on. Lowering the market share price , punishing those who rejected and offering a lower offer next time ?

This plagues me which makes me more incline to just accept.

While that is certainly within the realm of possibility, I’d like to think that ARA’s board is way above doing anything like that.

Besides, the long-term value of a stock is based on an amalgamation of factors (its underlying assets, growth, etc.), not just dividends. If ARA’s underlying value continues to grow into the future, investors, like you and I, will see and recognize that value 🙂

Case in point: Berkshire’s share price is US$234,860.00 and has only ever paid a dividend once.

I am a shareholder and I will be voting to reject this offer as this offer price is way too low. The reason is very well explained by Rusmin.

This deal will be done through a scheme of arrangement (SOA) and one of the process of the votes goes by headcount rather than the number of shares, that is regardless of whether the shareholder holds 1 share or 1,000,000 shares, the shareholder will only get 1 vote. Under this process, the minority shareholders certainly have a plausible chance to reject this deal.

The board of directors and management has been prudent so far, not to mention they are holding substantial shareholding in the company along with Straits Trading. Thus it would not seem to be plausible for dividends to be stopped. If this deal is rejected, it is likely that the next offer price would be higher going by other case studies.

As mentioned elsewhere, there’s a flaw in the author’s calculation. It needs to take into account the bonus and rights issue since 2013’s $1.80, and also the generous dividends that ARA is known for paying when calculating returns

I as a shareholder rather accepting the offer. If the offer didn’t go thru, the stock price must be falling by at least 20 to 30%. How long does the investor to recover the loss? it will forgo the opportunity cost to invest the fund getting from the offer..

I will definitely accept the offer to have a win win situation.

I think the author forgot about the $1 rights issue in 2015 and 1-for-10 bonus issue in 2012. Your position definitely still solidly above water, though having bought at an inflated price back then you’re not seeing terrific profits

Thank you for a great analysis of ARA. I am also a shareholder and was greatly sadden by the news of privatisation, but was excited again when I saw your wonderful comment. Yes, I will voted against it as well. While there are some gain in liquidating and profiting from this privatisation, as a value investor, I am sadden to see yet another good company being privatised. Indeed I agree with the author that this company is unique and one of a kind. Over the years, she was able to gather more funds (akin to good performance and gain confidence of private investors) to start and manage more REITS and Private entity. If one had check some of the REITS they managed, one will also noticed that their REITs have been buying more buildings during the last 2 years, ie still growing their AUM. So even if the deals do not go thru, and speculators may affect the share price by 20%-30%, I personally do not foresee that ARA as a company will perform badly given their good track record for the last many years.

My comments as published on another article are reproduced for easy reference.

Taking private undervalued companies may be referred to as PIRATIZATION and may also be perceived as ‘legal frauds’. This may be common in many countries.

It may be a common practise for some substantial/controlling shareholders not to equitably reward shareholders by giving dividends which may be substantially lower than the achieved profits resulting in low share prices which do not reflect the value of the company assets. This then thus enable the substantial/controlling shareholders to take the company private and enjoy the full market value of the company assets.

This is well illustrated by the above comment voiced at the AGM:

He said: “I think in your heart, you are buying us up because you know this is going to worth much more in the future. Maybe even $5 a share might not be too low. You offered us a small carrot and show us to the exit sign. I think it is not fair for long-term shareholders.”

Similar cases have been suspected to have happened in some land assets rich Malaysian companies.

Such a situation can only arise when there is co-operation [or may be more appropriately be perceived as collusion’] among the parties involved and the experts who give their advice to support such ‘privatizations’ who may claim to be ‘independent’ but it is common perception that one must support the one who pays you for your services. Such partisan actions may also be due to weak procedures or laws which may not provide for fairness.

IN SUCH CASES IT MAY BE APPROPRIATE TO SUSPEND TRADING OF SHARES ON A PARTICULAR DATE AND THEN ANNOUNCE ‘DISPOSAL OF ALL THE ASSETS IN THE OPEN MARKET AND THE PROCEEDS DIVIDED AMONG THE ENTITLED SHAREHOLDERS. ALTERNATIVELY THE PRIVATISATION SHARE PRICE SHOULD BE BASED ON CURRENT MARKET VALUE OF THE REAL ESTATE ASSETS.

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

If the offer of $1.78 is rejected then there is nothing to stop the controlling shareholders from not giving any dividend and let the share price go down and it is this power the controlling shareholder has over the others to ensure that they accept the offer or be possibly ‘punished/’penalized’ via further downside of share price.

AND ALL THIS MAY BE LEGAL AND IN ACCORDANCE WITH THE PRESCRIBED PROCEDURES OF THE REGULATORY AUTHORITIES.

It is common in many countries as it is a common perception that laws may be biased in favor of the rich as they can also have the financial resources to get the most expensive experts to defend their positions.