Founded in 1960, Malayan Banking Berhad (Maybank) has grown over the decades and now has a physical presence in 18 countries, including all 10 nations in Southeast Asia. Presently, Maybank is the largest integrated financial services group in Malaysia and the fifth largest in Southeast Asia based on market capitalisation (RM102.8 billion as at 6 May 2019) and remains the only Malaysian stock to exceed the RM100 billion mark.

I recently received and reviewed its latest 2018 annual report. Hence, I’ll be covering its latest financial results and valuation figures. Here are 12 things that you need to know about Maybank before you invest:

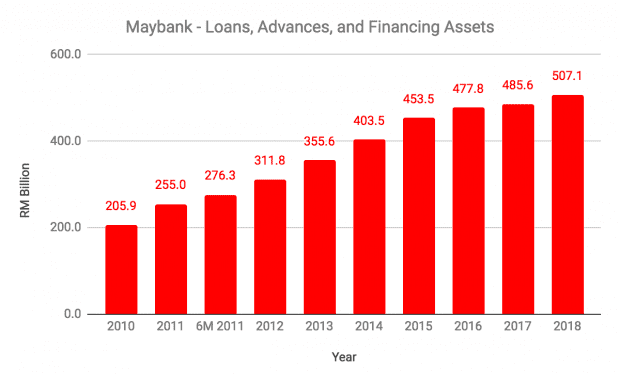

1. Loans, advances, and financing assets grew 4.4% year-on-year to RM507.1 billion in 2018, up from RM485.6 billion in 2017. This is attributable to a continuous rise in Maybank’s home markets — Malaysia, Singapore, and Indonesia — in its key segments such as mortgage, auto financing, and term loans and overdrafts to SMEs for the year.

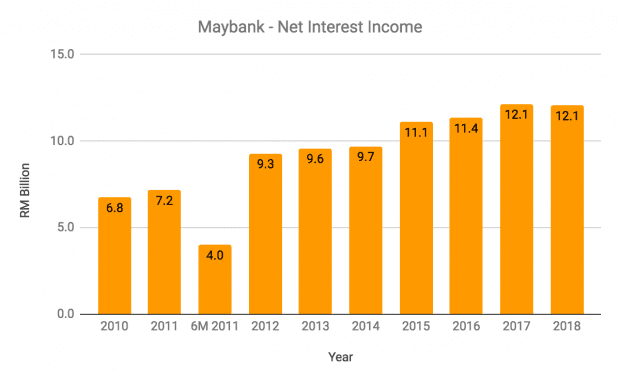

2. Net interest income maintained at RM12.1 million in 2018, a negligible drop of 0.6% from 2017. Maybank’s growth in interest income was due to an increase in LAF assets which was offset by an increase in interest expenses paid to deposits.

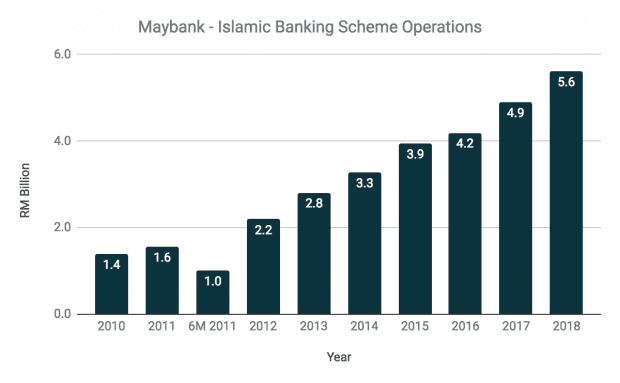

3. Islamic banking scheme (IBS) operations grew 14.5% year-on-year to RM5.6 billion in 2018 from RM4.9 billion in 2017. This is attributable to its continuous increase in financing assets for the year. Presently, IBS is the fastest growing division of Maybank, which is in line with Malaysia’s rapid developments in Islamic finance over the past 10 years.

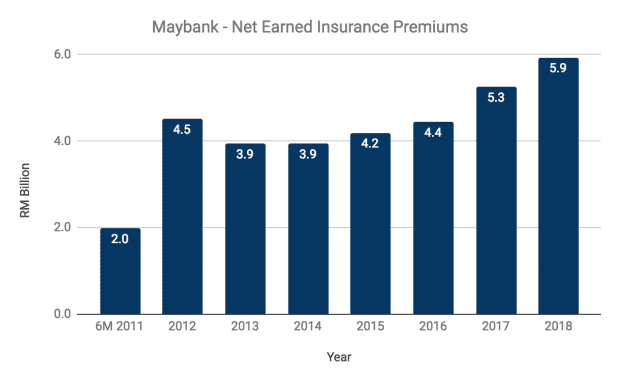

4. Net earned insurance premiums (NEIP) increased 13.0% year-on-year to RM5.9 billion in 2018, up from RM5.3 billion in 2017. This is attributable to strong growth from sales of bancassurance products, improved sales from its agency force in life and takaful products, and the broadening of online distribution channels to sell insurance products via RinggitPlus and MyEG.

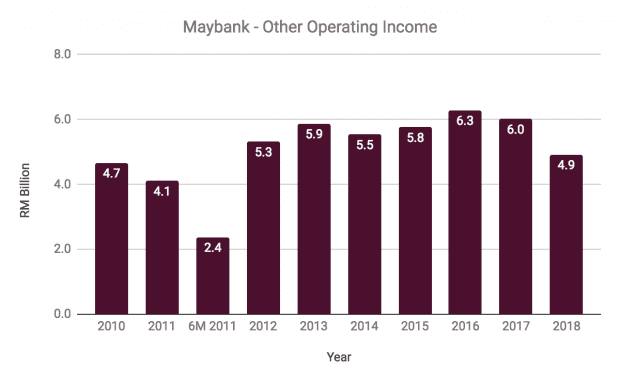

5. Other operating income dropped 18.4% year-on-year to RM4.9 billion in 2018 from RM6.0 billion in 2017. This is due to a net loss of RM431.7 million from investment activities in 2018 compared to a net gain of RM933.4 million from investment activities the year before. Maybank also recorded lower fee income and dividend income as a result of a weaker equity market in 2018.

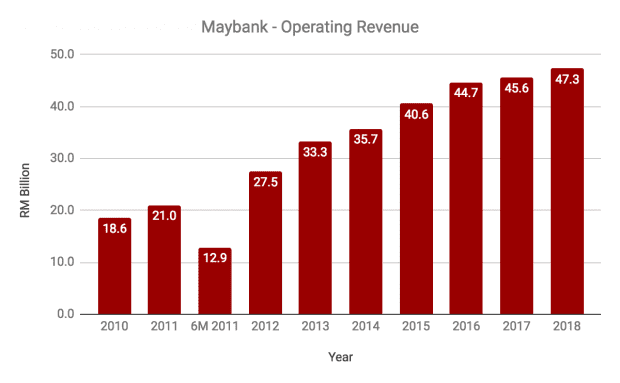

6. Overall, Maybank increased its operating revenue by 3.8% year-on-year to RM47.3 billion in 2018 from RM45.6 billion in 2017. This is mainly due to Maybank’s strong growth in IBS and NEIP in 2018.

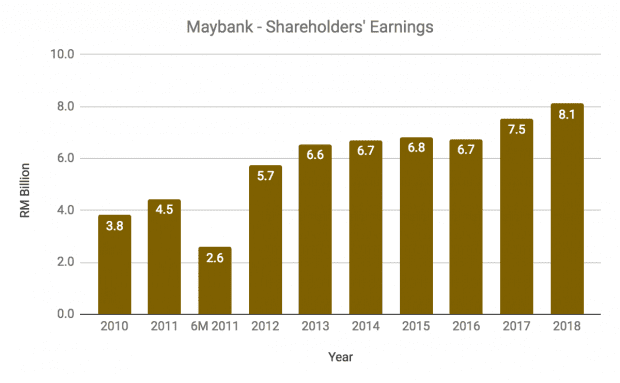

7. Shareholders’ earnings increased by 7.9% year-on-year to RM8.1 billion in 2018, up from RM7.5 billion in 2017. This is attributable to growth in operating revenue, a fall in impairment losses, and a stable cost-to-income ratio in 2018. Return on equity (ROE) increased for the second consecutive year from 9.8% in 2016 to 10.3% in 2017 to 10.8% in 2018.

8. Maybank maintained a healthy total capital ratio (TCR) of 19.0% in 2018, which is above the minimum requirement of 8.0% and additional capital buffer requirement of 2.5% from 2019 onwards. Maybank also has a healthy liquidity coverage ratio of 132.4%, well above the 90.0% minimum required by Bank Negara Malaysia. The two ratios indicate that Maybank is currently well-capitalised to remain solvent in the event of a significant financial stress scenario. Maybank has an ‘A-’ credit rating issued by S&P.

9. For 2019, Maybank aims to achieve an ROE of 11.0%, marginally more than the 10.8% recorded in 2018. It intends to achieve its target by sustaining balance sheet growth, increasing the sources of revenue through cross-business collaboration, and maintaining the quality of its assets. Maybank also aims to keep its cost-to-income ratio at 47% in 2019.

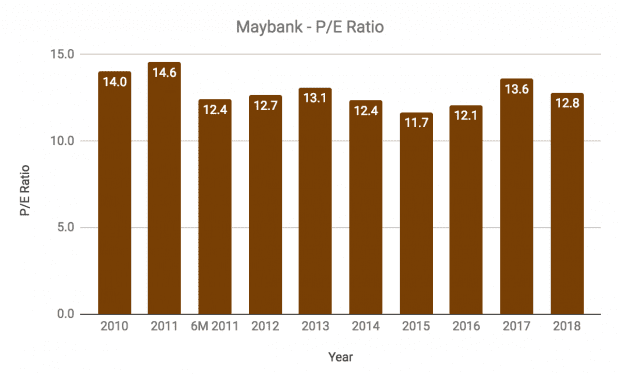

10. P/E ratio: As at 6 May 2019, Maybank is trading at RM9.30 a share. In 2018, it generated a total of RM0.742 in earnings per share. Hence, its current P/E ratio is 12.5, slightly below its 10-year average of 12.9.

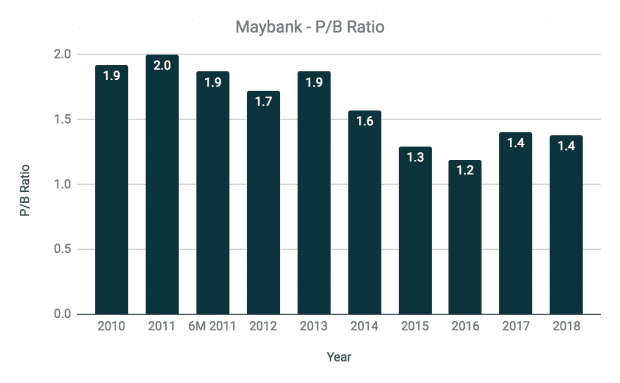

11. P/B ratio: As at 31 December 2018, Maybank has net assets of RM6.817 a share. Thus, its current P/B ratio is 1.36, which is lower than its 10-year average of 1.62.

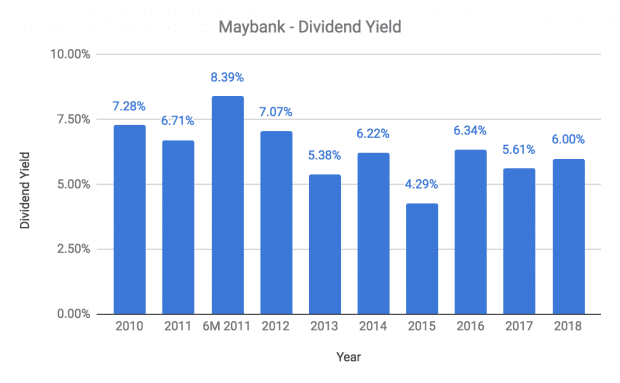

12. Dividend yield: Maybank has a dividend policy to pay out 40-60% of earnings as dividends. However, for the past 10 years, Maybank’s dividend payout ratio has consistently been above 70% due to its dividend reinvestment plan for shareholders. Maybank paid a dividend per share of RM0.57 in 2018. If Maybank maintains its dividend, its dividend yield is 6.1%, which is slightly lower than its 10-year average of 6.3%.

The fifth perspective

In summary, Maybank has continued to deliver sustainable growth in revenue, shareholders’ earnings, and dividends over the last 10 years. The bank is also well-capitalised with more than adequate capital and liquidity ratios. In terms of valuation, Maybank is currently trading below its historical averages and offers one of the highest dividend yields compared to other leading banks in Malaysia and Singapore.

Hi, thanks for the good write up.

My only concern is loan problem with Tuas Spring. What is your view on this?

Thanks

Hi RN,

Maybank has RM500+ billion in loans, advances, and financing. Its exposure to Tuas Spring (Hyflux) is RM1-2 billion. Let’s say Maybank wrote it off completely, will Maybank go bust? Will its earnings drop at a substantial rate? That’s up to investors (like you and me) to decide.