It’s the single most important metric people look for and demand, yet often subconsciously overlooked. We oftentimes make decisions not caring about what our potential return might be – we carelessly take what we see at face value and invest our money in it. Worse, we might not even try to calculate our potential return before deciding to invest.

“Oh look! SPH has dropped to multi-year lows similar to that of the financial crisis, I’m jumping in!”

Sound familiar?

While this decision may (or may not) yield good return, at the point in time when we haphazardly decide to invest, why weren’t we thinking more on the lines of: “What are the potential returns I can earn from this risky investment into SPH at today’s price?”

Understandably, it is incredibly tough and it takes arduous work to calculate an actual number out, for returns are essentially an estimation. We often disregard simple (or complex) returns calculations when prices become attractive to us, this may have no doubt yielded great results for some due to the margin of safety a price drop brings us, but the myopic focus on just this one security’s price may have cost us tremendously in opportunity costs.

In the local context, too many people have made investment decisions based on the face value of a piece of paper (or a massive tome) without caring so much as researching alternatives that provide similar or oftentimes better returns.

Let’s look at some examples.

Insurance-linked investment products

An agent of an insurer would offer you a plethora of investment ideas, an example could be that of a three-year 2% endowment plan. To the average layman, it could seem like a good deal considering that the interest earned in a savings account at the bank offers less than 1%. Many people thinking on this line would likely sign away their monies on the spot, without considering:

- This plan doesn’t have the same liquidity profile as a savings account which you can withdraw at any time.

- This plan is backed by the insurance company, but is perhaps less creditworthy than the bank. And if the sum of money invested is less than S$50,000, it is not insured by the Singapore Deposit Insurance Corporation.

Risk typically increases with returns and when the layman compares two completely different risk profiles and arrive at the decision to invest in a riskier product just for higher returns, he will have no one to blame but himself if something goes wrong.

Government bonds

The current U.S. Treasury 10-year yield sits at 2.35%, and the U.S.’s credit rating is just a notch below AAA by S&P, AAA by Fitch and Aaa by Moody’s. In contrast, the UK 10-year gilt sits at 1.32%, and the UK is rated AA with a negative outlook by S&P, AA- by Fitch and Aa2 by Moody’s.

What this means is, by investing in a 10-year bond issued by the UK government, you get less money in returns and assume more credit risk than investing with the U.S. Treasury. Seasoned bond investors might cite forex as the differential, but the sterling is just as weak as the dollar, so you get hit by forex losses too.

Institutional investors mandated to buy bonds might be one of the driving factors behind the active demand for UK gilts, but as a retail investor, this investment seen from a simplistic point of view does not make any sense.

Comparing across asset classes

As a benchmark, let’s take the two, five, and 10-year Singapore government bond yielding at approximately 1.42%, 1.69%, and 2.21% as of September 2017 respectively.

You come across an insurance-linked product that an insurance agent is trying to sell you, the policy that’s “guaranteed” by the insurer offers perhaps 2% yield over three years. As we all know, not all policies are created equal and many have actually performed far worse than their indicated yields. But taking it at face value, it may seem attractive to someone looking for a short-term alternative to a bank’s fixed deposit.

For this additional risk you’re taking, is it worth a spread of less than half a percent over a AAA-rated sovereign bond? One is backed by an insurer, the other is backed by the full faith and credit of a government. This is the question that may seem obvious but many seem to lack asking themselves before they invest.

For the investor with a riskier appetite, take stocks for example. If the dividend and share buyback yields have plunged because share prices have run up so high that the spread between the shareholder return yield and a government bond is maybe just 1% to 2.5%, is the extra risk worth it? Is the market frothy? Is this company worth paying so much for?

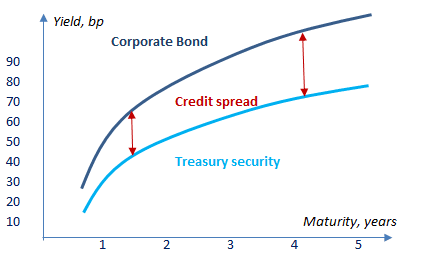

Junk bonds are a simpler gauge as their credit rating is, well, junk. Their credit spreads over U.S. treasuries is measured and published frequently. As of today, the spread is around 350 basis points. Is it worth the risk just to earn 3.5% more in a junk bond over a treasury bond?

When investors reach for yield in a low interest rate environment, they sometimes neglect the simple act of asking themselves how big of a spread between a risk-free bond and their investment is. This is when risk management is often thrown out the window, and investors often find themselves holding time bombs.

The fifth perspective

To sum up, price alone isn’t a reason to invest in any asset. Just because something is cheap means you’ll make a return — it’s important to remember there is risk in any investment and to ask yourself if your potential returns outweigh your risks. To take it a step further, for the same amount of risk you take, are there alternatives where you can earn a potentially higher return? As capital allocators, we want to maximise the returns on our wealth whenever possible.

Good article for those who do not know how to compare returns from different asset classes. But in the current investment where hostilities are about to break out between the US and north Korea, it is made more difficult to arrive at a decision.